Guardian Metal Resources PLC Announces Pilot Mountain Pre-Feasibility Study Results

Positive Pre-Feasibility Study Results for the Pilot Mountain Tungsten Project

PFS Completion marks a critical step toward restoring domestically mined tungsten production in support of the U.S. defense industrial base and national security priorities

At Base Case, Study Shows After-Tax NPV of US$660.3M and IRR of 59.6%

LONDON, UK / ACCESS Newswire / June 30, 2026 /Guardian Metal Resources plc (NYSE.A:GMTL)(LON:GMET)(OTCQB:GMTLF), a strategic exploration company focused on tungsten in Nevada, USA, is pleased to announce the results of the Pre-Feasibility Study ( "PFS " or the "Study ") for the Pilot Mountain tungsten project ( "Pilot Mountain " or the "Project "). The completion of the PFS marks a critical step in the Company 's path towards the potential development of the first new United States ( "U.S. ") based tungsten mining operation in over a decade.

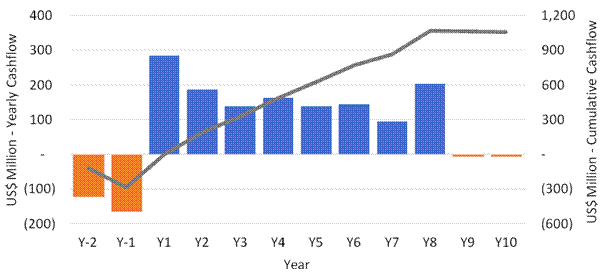

The Study results indicate that utilizing a conventional open-pit mining method and base case tungsten pricing*, the Project is planned to produce 15,916 tonnes of WO3 over an 8-year mine life, generating after-tax free cash flow of US$1.058 billion, with a capital payback period of 1 year from first commercial production. On an after-tax basis at base case tungsten pricing*, this translates to a net present value ( "NPV8 ") of US$660.3 million at an 8% discount rate and an internal rate of return ( "IRR ") of 59.6%. At the 12 June 2026 tungsten spot price, the Project would generate after-tax free cash flow of US$2.088 billion, with an IRR of 101.6%, an NPV8 of US$1.366 billion and a capital payback of 6 months from first commercial production.

The PFS was completed in accordance with S-K 1300 standards by a team of U.S.-based specialist firms, led by Samuel Engineering, Inc. of Denver, Colorado and RESPEC Company LLC ( "RESPEC ") of Reno, Nevada. The PFS includes an updated Mineral Resource Estimate ( "MRE ") covering two Project zones, Garnet and Desert Scheelite, as well a Mineral Reserve Statement ( "MRS ") for the Project. The supporting technical analyses relating to the updated MRE and MRS will be included in a S-K 1300 Technical Report Summary currently being prepared by the Company.

The Pilot Mountain PFS was made possible by a U.S. Department of War $6.2M Defense Production Act (DPA) Title III investment in Guardian Metal 's wholly-owned subsidiary, Golden Metal Resources (USA) LLC in July 2025. The Company sincerely thanks the Assistant Secretary of War for Industrial Base Policy, the Honorable Michael P. Cadenazzi, who oversees the Department 's execution of its DPA authorities, for their valued support of this milestone study, which marks a critical step toward restoring domestic tungsten mine production in support of the nation 's defense industrial base and national security priorities.

Currency values are stated in U.S. dollars and are presented on a 100% project basis. All tonnages are stated in metric tonnes.

*Base case utilizes a tungsten price of US$197,300 per tonne of WO3, representing a ~35% discount to the mid-price for ammonium paratungstate ( "APT ") as quoted by Fastmarkets MB-W-0001 of US$304,000 per tonne of WO3 as of 12 June 2026. The mid-price as of 26 June 2026 was US$307,500 per tonne of WO3. All prices are for APT with the study assuming a payable factor of 82% for tungsten concentrate.

Oliver Friesen, Chief Executive Officer of Guardian Metal, commented:

"We are delivering this Study at an inflection point: we believe that the global tungsten market is undergoing an unprecedented structural reset, and the world is waking up to the immense importance of securing reliable, home-grown critical mineral supply. The importance of tungsten for defense, technology, aerospace, and national security has never been more apparent. We believe that Pilot Mountain is the only tungsten Project in the United States with a recently completed S-K 1300 compliant PFS, positioning it as a unique opportunity for near-term U.S. mined tungsten production.

"Against this backdrop, the Pilot Mountain PFS supports the Project 's development potential to support U.S. critical mineral and defense independence. We believe this firmly establishes the Project as one of the more compelling tungsten development opportunities in the Western world. The Study demonstrates robust economics using conservative pricing assumptions, with considerable upside at current tungsten prices and from the Project 's exploration potential.

"The completed PFS is a testament to years of diligent work by our fantastic operations and development team, and gives us and our stakeholders great confidence as we advance the Project through further engineering, permitting and development toward a future construction decision. We look forward to sharing further updates as we progress toward establishing the first new domestically mined U.S. tungsten operation in over a decade, with production targeted for Q4 2028. "

Marc Leduc, P.Eng., Operations Manager of Guardian Metal, commented:

"This PFS represents the culmination of years of detailed technical work, and I am very proud of what our team has delivered. Tungsten is a metal critically important to U.S. defense, national security and reindustrialization, yet there has been no domestic production in the country for over a decade. Pilot Mountain is a high-margin Project that is uniquely positioned to fill a critical gap in the U.S. tungsten supply chain.

"We are particularly encouraged by the simplicity of the Project. We are proposing the use of conventional mining and processing methods throughout, producing what we believe will be a high-quality concentrate capable of being processed entirely within the U.S.

"The Study outlines a robust operation with a payback period of one year. Beyond the current resource base, we believe there is meaningful exploration upside across a number of the Project 's other target areas, including but not limited to, the Tremor Zone, Gunmetal, and Good Hope. We look forward to continuing to advance those targets alongside the important permitting and development work progressing on the Project 's Desert Scheelite and Garnet deposits. We believe that we are well positioned to file our Mine Plan of Operations in the near-term as we advance through the National Environmental Policy Act permitting process. "

PFS Highlights:

Economics, Pricing and Capex

• | After-tax NPV8 of US$660.3 million and Project IRR of 59.6%, with a capital payback period of 1 year generating after-tax free cash flow of US$1.058 billion*. |

• | Expected low initial Project capital expenditure ( "capex ") of US$288.7 million, with sustaining capital of US$33.9 million and closure costs of US$22.3 million. Capex includes 15.7% contingency (US$39.1 million) and US$34.3 million of preproduction mining. |

• | In its first full year of operations, the Project is modeled to generate US$348 million in Earnings Before Interest, Taxes, Depreciation, and Amortization ( "EBITDA ") at the base case*. |

• | As of the 12 June 2026 tungsten spot price of US$304,000 per tonne, first year EBITDA is modeled to increase to US$569 million, representing an uplift of approximately 64% from the EBITDA base case price. |

• | Also at the 12 June 2026 tungsten spot price, the Project generates after-tax free cash flow of US$2.088 billion with a 101.6% IRR and NPV8 of US$1.366 billion and has a capital payback period of 6 months from first commercial production. |

• | Expected adjusted operating cost of US$54,622 per tonne of WO3 in concentrate (including royalties, transportation, refining along with zinc and silver credits), with a targeted concentrate grade of 60% WO3. |

*Base case utilizes a tungsten price of US$197,300 per tonne of WO3, representing a ~35% discount to the mid-price for APT as quoted by Fastmarkets MB-W-0001 of US$304,000 per tonne of WO3 as of 12 June 2026. The mid-price as of 26 June 2026 was US$307,500 per tonne of WO3. All prices are for APT with the study assuming a payable factor of 82% for tungsten concentrate.

Resource, Reserve and Production

• | Mineral Resources increased to 21,600 tonnes of WO3 Indicated, with Probable Mineral Reserves of 20,275 tonnes of WO3 (11,822,000 tonnes @ 0.171% WO3). |

• | The operation plan calls for the construction of a 4,000 tonne per day processing plant using flotation recovery methods to produce a tungsten concentrate. |

• | The ore will be mined from a conventional open-pit mine using 92-tonne haul trucks and large wheel loaders. |

• | The operation plan calls for the construction of a conventional lined tailings storage facility which will meet the U.S. and international standards for tailings management, including the Nevada Administrative Code requirements and Canadian Dam Association guidelines. |

Timelines, Life of Mine, Permitting and Utilities

• | The Project timelines contemplate an open-pit mining operation with first ore through the mill in Q4 2028, with initial commissioning tonnes marking the start of processing operations. |

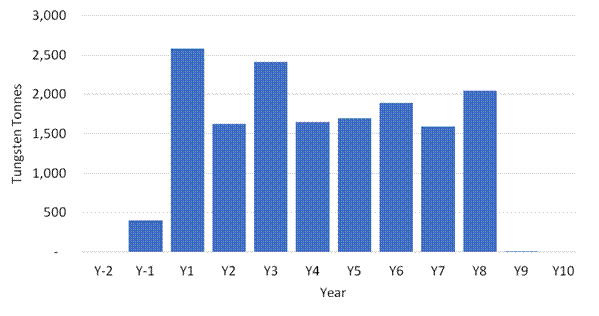

• | Expected initial 8-year Life of Mine ( "LoM ") producing 15,916 tonnes of recovered WO3, with significant opportunity to extend through ongoing exploration at the Tremor Zone, Gunmetal, Good Hope, plus other unnamed target areas across the Project. |

• | Work completed for the PFS supports the near-term filing of the Mine Plan of Operations ( "POO ") with the Bureau of Land Management as part of federal National Environmental Policy Act ( "NEPA ") permitting process. |

Investor Presentation:

As previously announced, Guardian Metal will host a live investor presentation via 6ix on 01 July 2026 at 11:00 ET / 16:00 BST to discuss the PFS results and provide an update on the Company 's outlook, including next steps for the Pilot Mountain Project.

The presentation is open to all existing and potential shareholders. Questions may be submitted ahead of the event via the registration form or at any time during the event.

Investors can sign up to 6ix for free and register for Guardian Metal 's presentation here: https://6ix.com/event/guardian-metal-resources-presents-pilot-mountain-pfs

PFS Summary Results with Price Sensitivities:

Item (all after tax) | NPV8 | IRR | After tax Cash Flow | Payback |

(US$M) | (%) | (US$M) | (years) | |

Base Case US$197,300/t WO3 | $660 | 59.6% | $1,058 | 1.00 |

Spot US$304,000/t WO31 | $1,366 | 101.6% | $2,088 | 0.51 |

Base -20% US$157,840/t WO3 | $395 | 41.3% | $671 | 1.31 |

Base +20% US$236,760/t WO3 | $922 | 76.0% | $1,440 | 0.71 |

Notes:

1. APT mid-price as of 12 June 2026 as quoted by Fastmarkets MB-W-0001. Latest price as of 26 June 2026 was US$307,500/t.

Further Details:

The following information is derived from the PFS. The PFS reflects a pre-feasibility level assessment of the Project, with the accuracy being plus 20% and minus 15% and is based on the assumptions and parameters described herein. References to "will " or "expected " reflect the planned development scenario, subject to a positive construction decision and successful Project financing.

The PFS envisages initial capital expenditure of US$288.7 million to construct a fully integrated mine, mill complex and associated infrastructure, with a mill feed capacity of 1.4 million tonnes per annum. The operation is designed to produce ~2,000 tonnes of WO₃ in concentrate per annum, with the targeted concentrate grade of greater than 60% WO₃ over the life of mine.

Adjusted operating costs are projected at US$54,622 per tonne of WO₃ contained in concentrate; AISC of US$58,151 per tonne of WO₃ contained in concentrate.

The economic analysis presented in the PFS is based on the assumptions and parameters used in the Study and should be read together with the qualifications, assumptions, and risk factors described elsewhere in this announcement.

The Desert Scheelite and Garnet tungsten deposits are located approximately 2 kilometers apart within a large land package hosting multiple areas of tungsten mineralization. Known tungsten intercepts proximal to the current resource areas provide meaningful potential for further resource expansion.

The PFS estimates first production in late 2028, subject to approval of the POO and a NEPA analysis in mid-2027. The Study utilizes conventional open-pit mining and processing methods, with mine design incorporating environmental protection measures across all phases of construction, operations, and closure. Grid power connection is anticipated via a potential self-build powerline option, with water supply to be sourced from wells, subject to receipt of the required water rights.

Combined production from two concurrent open pits is estimated at 15,916 tonnes of WO₃ in concentrate over the mine life, with a life-of-mine stripping ratio of 12.6, a head grade of 0.171% WO₃, and tungsten recovery from milling and flotation estimated at 78.5%. Mining will utilize 92-tonne haul trucks, with both contractor and owner fleet options evaluated in the PFS. The base case assumes a contractor mining model with an owner 's team management structure.

Initial mining of the Desert Scheelite pit will facilitate construction of a modern, zero discharge lined tailings storage facility with a rock embankment. Processing infrastructure will comprise primary and secondary crushing, a two-stage grinding circuit, and a flotation recovery plant. Tungsten will be recovered using an industry-standard fatty acid flotation circuit, with sulfide minerals, including silver, recovered ahead of the tungsten recovery stage. Silver will be produced as part of a base metal concentrate and marketed separately from the primary tungsten product.

PFS Detailed Technical Results:

Desert Scheelite | Garnet Tungsten | Total Pilot Mountain | ||

|---|---|---|---|---|

Study Production Statistics | Units | Mine | Mine | Project |

Total Ore Mined | million tonnes | 9.738 | 2.085 | 11.822 |

Total Material Mined | million tonnes | 144.013 | 16.337 | 160.350 |

Stripping Ratio | waste: ore | 13.8:1 | 6.8:1 | 12.6:1 |

Processing Rate | tonnes per day | 4,000 | ||

Tungsten Head Grade | % | 0.182 | 0.120 | 0.171 |

Silver Head Grade | Ag g/t | 10.68 | 2.78 | 9.28 |

Contained Tungsten | Tonnes WO3 | 17,768 | 2,507 | 20,275 |

Contained Silver | kOz | 3,343 | 186 | 3,529 |

Tungsten Recovery | % | 78.5% | 78.5% | 78.5% |

Silver Recovery | % | 60% | 60% | 60% |

Total Recoverable Tungsten 1 | Tonnes WO3 | 13,948 | 1,968 | 15,916 |

Total Recoverable Silver | kOz | 2,006 | 112 | 2,117 |

Average Annual Tungsten Production | Tonnes WO3 | 1,744 | 246 | 1,990 |

Average Annual Silver Production 2 | kOz | 251 | 14 | 265 |

Capital | ||||

Initial Capital | US$ million | $288.7 | ||

Sustaining Capital | US$ million | $33.9 | ||

Life of Mine Capital | US$ million | 322.6 | ||

Contingency (included) | US$ million | $39.1 | ||

Contingency (included) | % | 15.7% | ||

Operating Costs | ||||

Adjusted Operating Cost per Tonne of Ore 3 | US$/t ore | $73.54 | ||

Mining | US$/t ore | $48.16 | ||

Processing | US$/t ore | $24.86 | ||

G&A | US$/t ore | $6.23 | ||

Other 4 | US$/t ore | $(5.71) | ||

Adjusted Operating Cost per tonne of WO3 3 | US$/t WO3 net of by-products | $54,622 | ||

AISC per Tonne of WO35 | US$/t WO3 net of by-products | $58,151 | ||

Mine Life (LoM) | years | 8 | ||

Project Economics6 Base Case Pricing | ||||

Post-tax NPV (8%) | US$ million | $660.3 | ||

Pre-tax NPV (8%) | US$ million | $856.7 | ||

Post-tax NPV (10%) | US$ million | $589.6 | ||

Pre-tax NPV (10%) | US$ million | $767.5 | ||

Post-tax NPV (15%) | US$ million | $446.6 | ||

Pre-tax NPV (15%) | US$ million | $587.4 | ||

Post-tax IRR | % | 59.6% | ||

Pre-tax IRR | % | 67.8% | ||

Payback Period | years | 1.00 |

Notes:

1. WO3 calculations are made assuming a saleable good quality tungsten concentrate at >50% WO3 concentrate grade for the U.S. market.

2. Silver production is averaged over the Desert Scheelite mine life only.

3. Adjusted Operating Costs Include: On-site mining, processing and general and administrative expenses ( "G&A "), royalties and production/excise taxes, permitting and community cost related to current operations, third party smelting, refining and transport costs, stockpiles and inventory write-downs, site-based non-cash remuneration, and by-product credits.

4. Other category includes royalties, transport, production/excise taxes, refining, and by-product credit.

5. AISC includes: Adjusted Operating Costs (above) plus closure costs, and sustaining capital.

6. Project economics are presented for 100% of the project.

Figure 1: PFS Production Profile (Produced WO3 Contained in Concentrate)

Figure 2: PFS Post-tax Annual and Cumulative Cashflow Profile (grey line cumulative after tax cashflow - right axis)

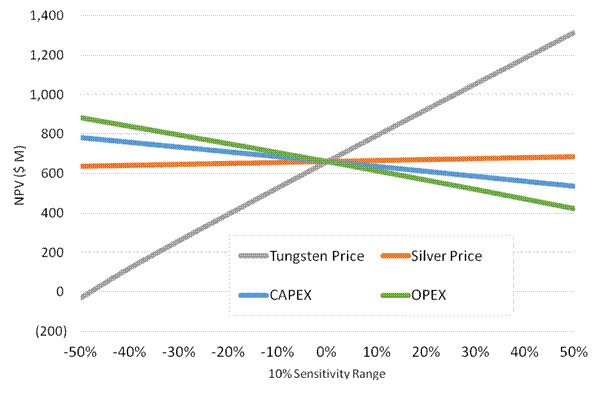

Figure 3: Project Sensitivity Analysis (Post-tax Base case NPV8 with 10% Sensitivities)

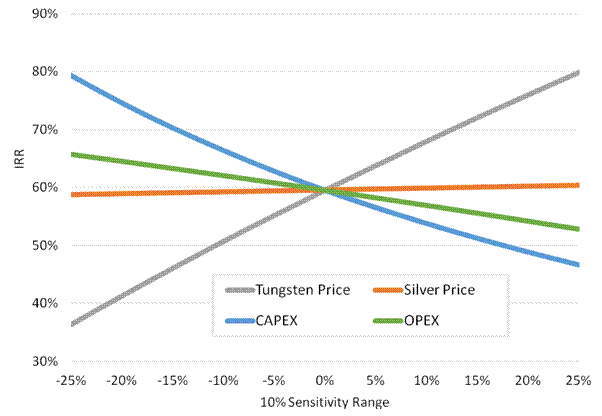

Figure 4: Project Sensitivity Analysis (Post-tax Base Case IRR with 10% Sensitivities)

EBITDA Calculation at Base Case Price

Metric | Unit | US$ |

Production | ||

Sold WO3 | tonnes | 15,916 |

Sold Zn | tonnes | 20,037 |

Sold Ag | ounces | 2,117,414 |

Revenue | ||

Total Gross Revenue | $000 | 2,702,949 |

Total Deductions | $000 | (6,335) |

Total Receipts less deductions | $000 | 2,696,614 |

Private Royalty (2%) | $000 | (54,059) |

Total Net Revenues | $000 | 2,642,555 |

Project Operating Costs | ||

Mining Cost | $000 | (569,318) |

Processing Cost | $000 | (293,902) |

SG&A Cost | $000 | (73,282) |

Total Operating Costs | $000 | (936,902) |

Project Capital Costs | ||

Project Development Capital | $000 | (288,701) |

Sustaining Capital | $000 | (33,929) |

Closure | $000 | (22,250) |

Total Capital Cost and Closure | $000 | (344,880) |

EBITDA, Capital, Tax and Cashflow | ||

EBITDA | $000 | 1,705,654 |

EBITDA-Capital | $000 | 1,360,773 |

Total Taxes | $000 | (302,684) |

After Tax Total Cashflow | $000 | 1,058,090 |

The Mineral Reserve and Mineral Resource estimates summarized below are derived from the PFS. The supporting technical analyses, assumptions, and disclosures relating to such estimates are expected to be included in a forthcoming Technical Report Summary being prepared in accordance with S-K 1300.

Pilot Mountain Project Mineral Reserve Statement:

Probable Reserves total 11.8 million tonnes containing 20,275 tonnes of WO3 and 3.5 million ounces silver as detailed below:

Average Grade | Contained Metal | |||||||

Pit | Classif-ication | k Tonnes | WO3% | Ag g/t | Zn % | WO3 t | K oz Ag | Zn t |

Desert Scheelite | Probable | 9,738 | 0.182 | 10.68 | 0.30 | 17,768 | 3,343 | 28,813 |

Garnet | Probable | 2,085 | 0.120 | 2.78 | 0.22 | 2,507 | 186 | 4,583 |

Total | Probable | 11,822 | 0.171 | 9.28 | 0.28 | 20,275 | 3,529 | 33,396 |

Mineral Reserve Statement Notes:

1. The effective date of Desert Scheelite and Garnet Mineral Reserve Statement is 15 June 2026.

2. The point of reference for Mineral Reserves is at the crusher.

3. Resource blocks were diluted to the selective mining unit (SMU) and additional dilution was added for reporting of Reserves. The QP, RESPEC, who is responsible for the statement of reserves believes that the blocks can be reasonably mined at the SMU size. Desert Scheelite SMU blocks were 5m by 2.5m by 5m in the X, Y, and Z directions respectively. Garnet SMU blocks were 5m by 5m by 2.5m in the X, Y, and Z directions respectively.

4. Reserves are reported based on a 0.040% WO3 cutoff grade. The cutoff grade was applied only to the WO3 grades. Silver and tungsten are reported as the contained metal within the Probable material processed.

5. Rounding may result in apparent discrepancies between tonnages and contained metal totals.

6. Indicated material has been converted to Probable Reserves. The resources do not contain any Measured material, so no Proven reserves are reported. All Inferred resources are considered as waste material.

7. Reserves are reported by RESPEC.

8. Reserves are reported based on US$115,000/t WO3, US$38.00/oz Ag, and US$2,700/t Zn metal prices. Note that the final cashflow analysis uses a higher WO3 price. The lower price is reasonable with the reporting of reserves as RESPEC considers material below the reporting cutoff grade to be immaterial.

Pilot Mountain Project Mineral Resource Estimate:

Mineral Resources are reported inclusive of Mineral Reserves. Indicated total 12.1 million tonnes containing 21,600 tonnes of WO3 and 3.9 million ounces silver as detailed below:

Average Grade | Contained Metal | |||||||

Pit | Classif-ication | k Tonnes | WO3 % | Ag g/t | Zn % | WO3 t | k oz Ag | Zn t |

Desert Scheelite | Indicated | 9,978 | 0.189 | 11.39 | 0.30 | 18,900 | 3,656 | 29,900 |

Inferred | 1,933 | 0.158 | 11.48 | 0.29 | 3,000 | 713 | 5,500 | |

Garnet | Indicated | 2,158 | 0.127 | 3.18 | 0.23 | 2,700 | 221 | 5,000 |

Inferred | 364 | 0.110 | 1.87 | 0.11 | 400 | 22 | 400 | |

Total | Indicated | 12,136 | 0.178 | 9.93 | 0.29 | 21,600 | 3,877 | 34,900 |

Inferred | 2,297 | 0.150 | 9.96 | 0.26 | 3,400 | 735 | 5,900 |

Mineral Resource Estimate Notes:

1. The effective date of Desert Scheelite and Garnet mineral resources is 26 May 2026.

2. The Mineral Resource estimate was calculated by RESPEC in metric tonnes.

3. The point of reference is in situ mineralization prior to extraction by open pit mining methods.

4. The average grades of the tabulations are comprised of the weighted average of block-diluted grades within optimized pits.

5. The Desert Scheelite and Garnet Mineral Resource cut‑off grade of 0.04% WO₃ was selected by the authors. Operating assumptions were applied to establish a theoretical pit limit, including a WO₃ price of US$115,000/t, an average recovery of 75% WO₃, a processing rate of 4,000 tonnes/day, US$3.50/t mining cost for open pit, US$23.00/t processing cost, US$5.17/t processed for G&A, and an 82% payability. Blocks outside the pit limit are considered not economic at this time.

6. The accessory metals Ag and Zn shown in the above table are the quantities contained within the Mineral Resource envelope using the cut-off grade established for the primary commodity (WO3). No independent cut-off grade has been applied to these accessory metals. Reported quantities of accessory metals are therefore considered by-products of the primary metal resource and their value is contingent upon the ability to economically extract the by-products along with the primary commodity.

7. The estimate of Mineral Resources may be materially affected by geology, environmental, permitting, legal, title, taxation, sociopolitical events, marketing, or other relevant issues.

8. Rounding as required by reporting guidelines may result in apparent discrepancies between tonnes, grade, and contained metal content.

9. Mineral Resources are not Mineral Reserves and do not have demonstrated economic viability. An Inferred Mineral Resource has a lower level of confidence than an Indicated Mineral Resource and cannot be converted to a Mineral Reserve. RESPEC reasonably expects that continued exploration and delineation will upgrade the majority of Inferred Mineral Resources to Indicated Mineral Resources.

Outlook:

The tungsten market has been fundamentally reshaped by the absence of domestic U.S. primary mined supply and China 's decision in February 2025 to control exports of tungsten raw materials, having historically accounted for approximately 80% of global primary supply.

Guardian Metal is committed to advancing Pilot Mountain as rapidly as possible, progressing detailed engineering and permitting activities in parallel as it works towards a construction decision. The Company is actively engaged with relevant government agencies and participants across the tungsten value chain, reflecting its view that the United States is facing a material near- and medium-term tungsten supply shortage. In addition, the Company will consider the best value of the Project for all stakeholders including local, state and national communities through the permitting and final designs.

Given the severity of the current supply deficit, the prevailing price environment, and strong modeled operating margin, the Company may elect to make a construction decision based on the 2026 PFS, potentially proceeding to production without completion of a full feasibility study. However, no such decision has been made at this time and further technical, permitting, financing, and development work remains ongoing. Readers are cautioned to consider this possibility when evaluating the Project and its associated risks.

Project Ownership:

Guardian Metal owns a 100% interest in Pilot Mountain through its U.S. wholly-owned subsidiaries Pilot Metals Inc. and BFM Resources Inc.

References

1 Company announcement, U.S. Department of Defense Awards US$6.2M to Golden Metal Resources for the Pilot Mountain Project, dated 23 July 2025

( https://polaris.brighterir.com/public/guardian_metal_resources/news/rns/story/wvm0n3w )

Qualified Person

Scientific and technical disclosure contained herein has been reviewed and approved by independent third-party consulting firms-RESPEC, Samuel Engineering, Inc., and NewFields Mining Design & Technical Services, LLC ( "NewFields ") -each a 'qualified person ' under Subpart 1300 of Regulation S-K. RESPEC has reviewed and approved the disclosures relating to exploration results, and Mineral Resource and Reserve estimations. Samuel Engineering, Inc. has reviewed and approved the disclosures relating to metallurgical testing, processing design, and economic analysis. NewFields has reviewed and approved the disclosure related to the Tailings Storage Facility. The findings and conclusions of the Study have not yet been formalized and summarized into a Technical Report Summary prepared in accordance with Subpart 1300 of Regulation S-K. The Company is currently preparing an updated Technical Report Summary reflecting the results of the Study and expects to file such Technical Report Summary with the SEC in the near-term. This announcement summarizes the principal findings and conclusions of the PFS. Additional technical information, assumptions, qualifications, and supporting analyses relating to the Mineral Resource estimates, Mineral Reserve estimates and economic analysis summarized herein are expected to be included in the forthcoming Technical Report Summary.

Independent Review Statements

The technical information contained in this disclosure has been read and approved by the U.S. Department of War and by Mr Nicholas O 'Reilly (MSc, DIC, MIMMM QMR, MAusIMM, FGS), who is a qualified geologist and acts as the Competent Person under the AIM Rules - Note for Mining and Oil & Gas Companies. Mr O 'Reilly is a Principal consultant working for Mining Analyst Consulting Ltd which has been retained by Guardian Metal Resources plc to provide technical support.

This announcement contains inside information for the purposes of Article 7 of EU Regulation 596/2014 (which forms part of domestic UK law pursuant to the European Union (Withdrawal) Act 2018).

Cautionary Note to Investors: Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability.

Forward Looking Statements

This announcement contains forward-looking statements relating to expected or anticipated future events and anticipated results that are forward-looking in nature, and, as a result, are subject to certain risks and uncertainties, including general economic, market and business conditions, competition for qualified staff, the regulatory process and actions, technical issues, new legislation, potential delays or changes in plans, uncertainties resulting from operating in a new political jurisdiction, uncertainties regarding the results of exploration, the timing and granting of prospecting rights, the timing and granting of regulatory and other third party consents and approvals, Guardian Metal 's or any third party 's ability to execute and implement future plans, and the occurrence of unexpected events.

Forward-looking statements are subject to risks and uncertainties, including those described in the Company 's filings with the SEC. There can be no assurance that the Project will be developed on the timetable contemplated by the PFS, or at all, or that the economic outcomes described in the PFS will ultimately be realized. Guardian Metal undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required by law.

This announcement does not purport to be full or complete. No reliance may or should be placed by any person for any purpose on the information contained in this announcement or its accuracy, fairness or completeness. The information in this announcement is subject to change. For further information visit www.guardianmetalresources.comor contact the following:

Guardian Metal Resources plc Oliver Friesen (CEO) | Tel: +44 (0) 20 7583 8304 |

Cairn Financial Advisers LLP Nominated Adviser Sandy Jamieson/Jo Turner/Louise O 'Driscoll | Tel: +44 (0) 20 7213 0880 |

Berenberg Joint Broker and Financial Adviser Jennifer Lee/Ivan Briechle | Tel: +44 (0) 20 3207 7800 |

Tamesis Partners LLP Joint Broker Charlie Bendon/Richard Greenfield | Tel: +44 (0) 20 3882 2868 |

Tavistock Financial PR in the UK Emily Moss/Josephine Clerkin | Tel: +44 (0) 7920 3150 / +44 (0) 7788 554035 |

Edelman Smithfield Financial PR in the US |

About Guardian Metal Resources

Guardian Metal Resources PLC (NYSE.A:GMTL)(LON:GMET)(OTCQB:GMTLF) is a strategic mineral exploration company driving the revival of U.S. mined tungsten production and strengthening America 's defense metal independence. The Company is advancing two co-flagship tungsten projects, Pilot Mountain, one of the largest undeveloped tungsten deposits in the United States and Tempiute, formerly America 's largest producing tungsten operation, both located in Nevada, one of the top-rated mining jurisdictions in the United States.

In July 2025, the U.S. Department of War (DoW) under Title III of the Defense Production Act of 1950, as amended, invested US$6.2M in Golden Metal Resources (USA) LLC, a wholly-owned subsidiary of Guardian Metal Resources PLC, to support the Pilot Mountain PFS. The Company completed a U.S. listing on the NYSE American on 20 March 2026.

Tungsten is a strategic metal critical to the defense, energy transition, technology, and industrial sectors. In the context of shifting geopolitical dynamics and tightening Chinese export restrictions, Guardian Metal is well positioned to play a leading role in re-establishing a secure, domestically mined US supply chain for this vital defense metal.

This information is provided by RNS, the news service of the London Stock Exchange. RNS is approved by the Financial Conduct Authority to act as a Primary Information Provider in the United Kingdom. Terms and conditions relating to the use and distribution of this information may apply. For further information, please contact rns@lseg.com or visit www.rns.com.

SOURCE: Guardian Metal Resources PLC

View the original press release on ACCESS Newswire

© 2026 ACCESS Newswire. All Rights Reserved.